“A quarter of the Dutch companies that are required to submit sustainability reports from January 1st 2024 do not collect the necessary data” – Research performed by SEO and the University of Amsterdam (UvA)

Starting book year 2024, organizations across Europe, and thus in the Netherlands, are required to report on their sustainability efforts, from policies to impacts. The obligation to report on this is the result of the Corporate Sustainability Reporting Directive (CSRD). Recent research conducted by the economic research agency SEO and the University of Amsterdam highlights that almost half of the organizations required to report on 2024 already continuously monitor their impacts, making it easier to gather data or report on sustainability at a later stage. Another 25 percent of these companies already gather data and report on their results and the other 25 percent thus does not collect any data at all, yet. Only 1 percent of companies is not concerned with the new reporting directive.

Current and future ingredients

The CSRD is the biggest change in the reporting landscape. However, the CSRD is not a separate framework disconnected from other laws and policies. The CSRD references, i.e., the EU Taxonomy several times and is interlinked with the sustainability reporting standards from the Global Reporting Initiative (GRI) and the standards from the International Sustainability Standards Board (ISSB). This blog is designed to make your organization aware of the ever-evolving alphabet soup of sustainability reporting.

We will dive into the different reporting aspects that might be applicable to your organization, outlining the key changes that occurred in 2023 and what to expect in 2024. But beware: understanding the interconnectivity between the different standards is crucial to help your company understand the function of the different reporting frameworks and how to implement their guidelines.

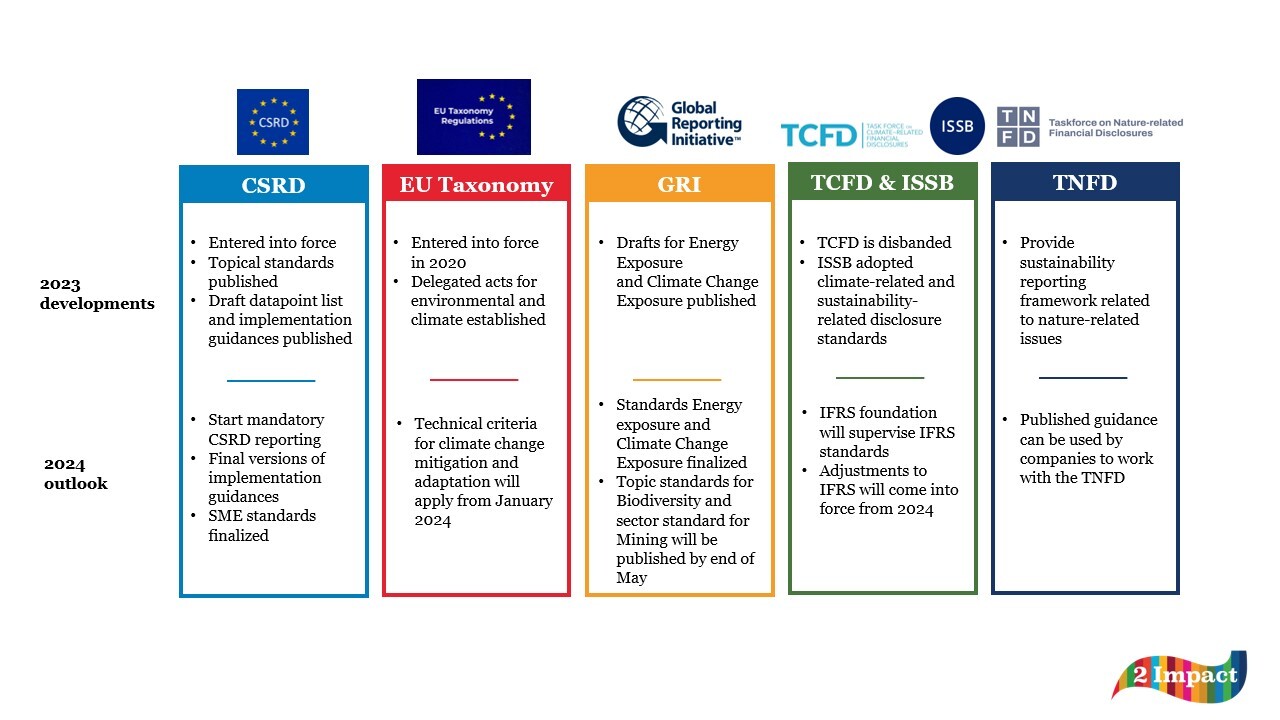

Corporate Sustainability Reporting Directive (CSRD)

On January 5th, 2023, the CSRD entered into force. Based on the earlier Non-Financial Reporting Directive (NFRD), the CSRD modernizes and presents a comprehensive picture of the reporting rules concerning social, environmental, and governance information. The requested information is split up into ten topical standards and two cross-cutting standards, laid out in the European Sustainability Reporting Standards (ESRS). These standards constitute of three layers:

- Sector-agnostic standards, applicable to all companies in scope

- Sector-specific standards, applicable to all companies in a specific sector

- Entity-specific standards, relating to yet uncovered topics relevant in the ESG landscape

What to expect in 2024?

The first batch of companies required to report under the CSRD, those that are in the scope of the NFRD, start reporting under the CSRD in financial year 2024, so in just a few weeks’ time. To simplify working with the ESRS, EFRAG published a supporting datapoint list and materiality assessment and value chain implementation guidance. These publication guidance documents are open for public consultation until the end of January- after which the final versions will be published. There is also a Q&A platform to clarify the CSRD and ESRS. Further, in 2024, a consultation will take place on the standards for Small and Medium-sized Enterprises (SMEs) and they will be finalized.

Currently, only the sector-agnostic standards entered into force, with the sector-specific standards expected to be published in 2026. In the meantime, companies can report entity-specific standards that are currently not included in the ESRS. Entity-specific standards do not follow a predetermined format.

The EU Taxonomy

The sustainability reporting realm also consists of the EU Taxonomy. Already entered into force in 2020, the Taxonomy is a market transparency tool to identify sustainable economic activities, i.e. economic activities aligned with the net zero by 2050 trajectory and other environmental objectives.

What to expect in 2024?

In 2023 some developments took place by the establishment of the delegated acts for environment and climate, stipulating the technical criteria for when an economic activity can be seen as contributing substantially to the sustainable use of water and marine resources, circular economy and the restoration of biodiversity and ecosystems, among others. Next to that, the technical criteria for climate change mitigation and adaptation have been updated. Both these sets of technical screening criteria apply from January 2024 onwards.

Link EU Taxonomy and ESRS: E1-1 Transition plan for climate change mitigation

Global Reporting Initiative (GRI)

As one of the leaders in sustainability reporting standards, the GRI cannot be excluded from this interconnective overview. GRI provides accounting and reporting standards on how to disclose information on environmental impact, economy and people.

In 2023, two topic standards were published: the draft for energy exposure and the draft for climate change exposure. The former focuses on the role of energy policies and commitments in the decarbonization transition and energy consumption and generation, both within the own organization and in the value chain. The latter, incorporates ‘just transition’ principles and provides guidance on disclosing climate change mitigation transition plans, emission reduction targets and disclosures on climate change adaptation, e.g. impacts on local communities and biodiversity.

Link GRI and CSRD: please see mapping document.

What to expect in 2024?

The Energy Exposure and Climate Change Exposure drafts will be converted into final publications in 2024. Additionally, after being reviewed by peers, the topic standard for Biodiversity and the sector standard for Mining will be published by the end of May 2024.

Taskforce on Climate-related Financial Disclosures (TCFD) and International Sustainability Standard Board (ISSB)

Over 8 years ago, the Task Force on Climate-related Financial Disclosures (TCFD) developed a framework to support organizations to disclose climate-related risks and opportunities more effectively. However, after publishing the 2023 status report on sustainability disclosures, the TCFD is disbanded. Based on the TCFD recommendations of the last few years, the International Sustainability Standards Board (ISSB) adopted climate-related and general sustainability-related disclosure standards, making the TCFD obsolete. These sustainability standards are not part of the bigger IFRS-framework.

What to expect in 2024?

From this moment on, the IFRS Foundation will continue to supervise and monitor the sustainability disclosures of companies using the IFRS-standards. Recently, some amendments to the IFRS were approved which will commence in 2024. For instance regarding transparency of supplier finance arrangements and their effects on companies. An overview of the amendments can be found here.

Link TCFD and CSRD: ESRS 2 IRO-1 – Description of the processes to identify and assess material climate-related impacts, risks and opportunities

Taskforce on Nature-related Financial Disclosures (TNFD)

Last September, the Taskforce on Nature-related Financial Disclosures (TNFD) – a science-based, market-led, and global initiative – published their sustainability reporting framework. This framework guides organizations to identify, assess, manage and report on nature-related dependencies, impacts, risks and opportunities (“nature-related issues”), consistent with global sustainability framework like the CSRD.

The TNFD, similar to the TCFD, includes disclosure recommendations structured around four pillars: governance, strategy, risk management, and metrics and targets. Besides, this initiative provides sector-specific guidance to support the LEAP approach assessment – an assessment on nature-related issues (i.e., for oil and gas, food and agriculture, and financial institutions).

Link TNFD (LEAP approach) and CSRD: ESRS 2 IRO-1 – Description of the processes to identify and assess material pollution-, water and marine resources-, resource use and circular-economy-related impacts, risks and opportunities

What to expect in 2024?

In 2023, the TNFD launched the final set of disclosure recommendations and guidance. Every company is different, and so the organization behind the TNFD has published a guidance for adopting the TNFD recommendations (Getting started with the TNFD Recommendations – TNFD). In 2024, this guidance can help you manage your nature-related issues which are crucial to incorporate in your sustainability efforts.

Start cooking

CSRD, EU Taxonomy, GRI, TCFD, ISSB and TNFD, you’ve been welcomed to this alphabet soup specially made for your organization. Some of them have been here for a while and others have only recently popped up during your Monday morning meeting.

Now you have had a little taste of what is all out there and what is yet to come. If you have not done so already, start adding your own ingredients – impacts, data, knowledge – to this pan. This leads to preparing a sustainability report to your organizations’, your stakeholders’ and to the legislator’s liking.

Esther De Graaf RC, Founder and Managing Director 2Impact